RELX PLC

A deeper look at RELX PLC

Company Description

RELX, listed as REL on the London stock exchange, is a global provider of information-based analytics and decision making tools for professional and business customers. Their goal is to help customers make better decisions, get better results and be more productive.

RELX operates in 4 segments:

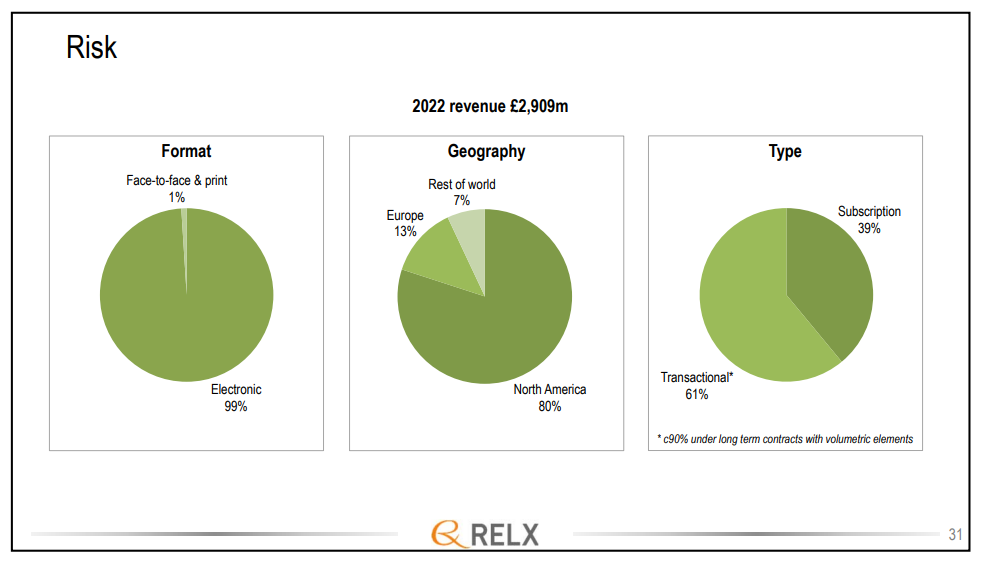

Risk ( 34%)

Scientific, Technical & Medical (34%)

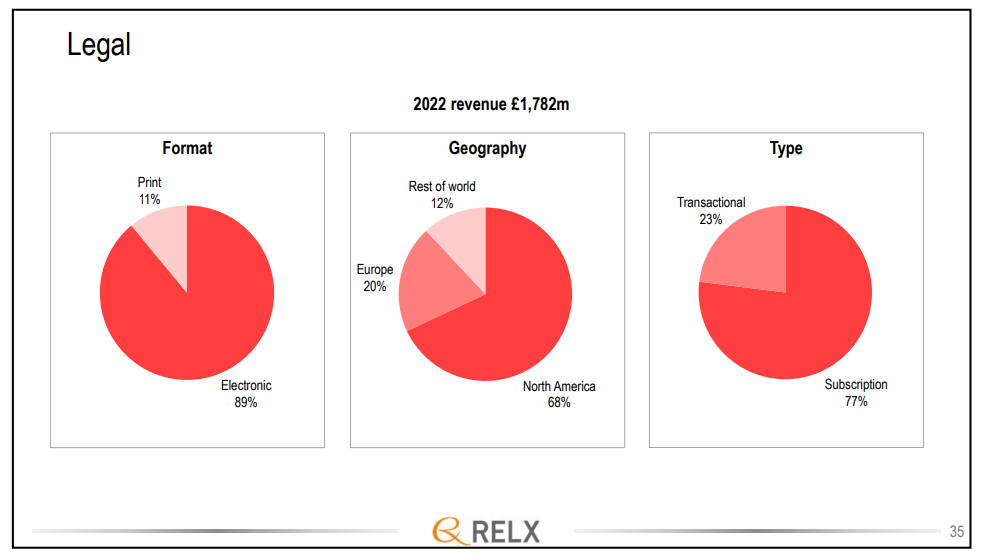

Legal (21%)

Exhibitions (11%)

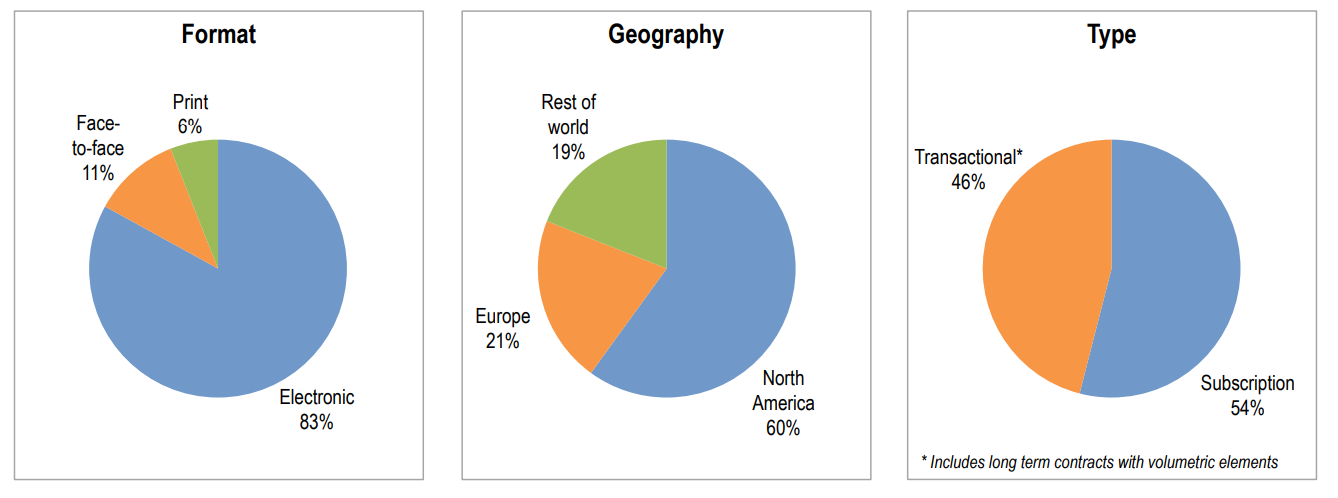

The products are generally sold through dedicated sales forces to customers and are priced on a subscription or transactional basis, normally under multi-year contracts. The services are provided in 3 reported formats, the data being provided in print and electronically formats and the exhibitions being reported as face to face. The company operates globally but earns a significant amount (60%) from North America.

RISK

The segment provides customers with information-based analytics and decision tools that combine public and industry specific content with advanced technology and algorithms to assist in evaluating and predicting risk and enhancing operational efficiency.

The segments revenue streams are:

Business Services (45%): Examples includes credit scores, fraud and identity solutions and cybercrime.

Insurance Services (40%) : Providing data for insurers use in assessing risk.

Specialised Industry Data Services (10%) : Data analytics for various sectors, for example aviation and agricultural.

Government Solutions (5%)

The segment deals mostly in direct to client sales, with Business Services and Insurance being mostly transactional with the Specialised Services and Government Solutions having a higher contribution from subscriptions.

Scientific, Technical & Medical

The segment helps researches and healthcare professionals advance science and improve health outcomes by combining information and datasets with analytical tools to facilitate insights and critical decision-making.

The various platforms provide customers with millions of published journals across the different sectors. The segment is the global leader in its market.

The segments main revenue streams are:

Primary research (50%) : This is provision of RELXs extensive journal library.

Databases, Tools and e-References (35%) : Here RELX provides a portfolio of products that combines structured data and advanced data science tools.

Legal

The segment provides legal, regulatory, and business information and analytics that helps customers increase their productivity, improve decision making and achieve better outcomes.

The primary tool offered in the legal market is LexusNexis. The site contains datasets, legal case studies, precedents, case studies and legal news.

The segment has a market position of second in the US and first outside the US.

Exhibitions

The segment combines industry expertise with data and digital tools to help customers connect digitally and face to face, learn about markets, source products and complete transactions.

Events include the Cannes Yacht Festival and NY Comic Con.

COVID decimated the segments earnings but the last two years has seen the segment starting to normalise.

Does RELX have a Moat?

As quality investors the competitive advantage (Moat) that a company possesses is one of the key aspects of a companies investment case.

Intangible assets and switching costs create RELXs moat/competitive advantage. The large majority of RELXs revenues are earned from the provision of data and analytics to clients. Over the years, RELX has developed sophisticated databases and decision making tools that many industries and professionals heavily rely on in order to carry out their daily activities. Two examples are:

In the Scientific, technical & Medical segment RELXs operates partly through Knovel, an online library that is used by 700 large clients, including 74 of the fortune 500 companies and hundreds of universities. Knovel is used in the engineering industry and offers guidance and best practice information on a huge range of materials, allowing engineers to quickly establish tolerances, environmental impacts and safety and compliance procedures, all in one place.

In the Legal segment, RELX has LexusNexis, the company’s flagship product. LexusNexis works across both the Legal and Risk segments. In Legal, RELX employs hundreds of legal professionals to review and update legal content to ensure it is current and comprehensive, resulting in a catalogue of extremely valuable resources that is core to RELXs moat.

In addition to the above, there are a few aspects to RELXs moat that relate to the high retention rate of clients. Firstly, there are nonfinancial switching costs that clients will experience if they were to change suppliers. Many of the operating systems and services offered by RELX require significant training and are heavily integrated within various professions. This leads to clients being reluctant to switch to an alternate provider, leading to high retention rates across the company.

Secondly, most of the services and systems provided by RELX represent a small portion of clients overall costs, for example in legal it can be only 1-2%, therefore it is not normally a place for clients to look when they are attempting to cut costs.

Finally, several of the industries that RELX operates are close to duopolies or oligopolies (specifically the legal information industry), and pricing normally is disciplined, this leads to little financial incentive for clients to switch providers.

Financial Analysis

Income statement

Looking at a high level, revenue growth has been slow over the last 3 and 5 years, as the company recovers from the pandemic period. For the 5 years leading up to the end of 2019, RELX grew it’s top line at a compound annual growth rate (CAGR) of 6,5%.

The pandemic saw a 70% drop in revenues from exhibitions, for obvious reasons, since then the segment has seen good growth, but remains 25% below 2019 levels. While the remaining segments did see some low growth in 2020, overall revenue dropped 9% in the year.

Recently released results saw revenue grow 9%, with Risk leading the way at 8% growth, this with the overall growth of 7% in 2021 saw revenue go above pre COVID levels and go above £8 billion for the first time.

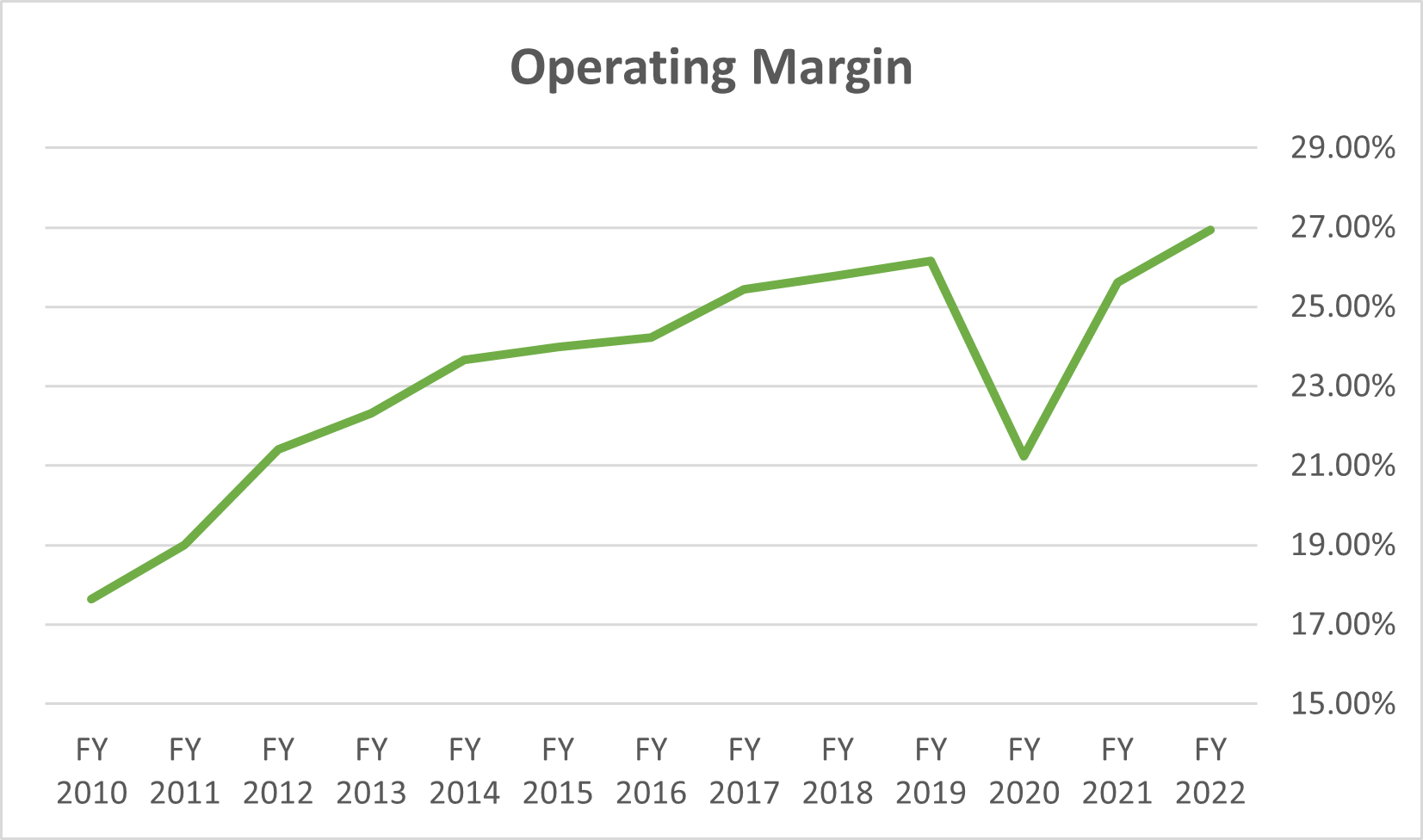

Up to the pandemic operating margin was seeing yearly expansion, this is attributed to the change in product offerings over the last decade where RELX has moved from the print offering into electronic. While the graph does indicate a drop in electronic contribution since 2020, as we mentioned above exhibitions revenues declined significantly during the pandemic, moving the contribution from 16% to 5%. The return of this segment in the last two years has increased its contribution back up to 11%, which has resulted in the continued move out of print to no be corrected represented. However it can be seen in the further expansion in operating margin, which is as of last results slightly under 30%, nearly 0,8% above 2019 levels.

RELXs earnings per share (EPS) is slightly above where it was in 2017, but that year saw an irregular Deferred tax income of over 3 times the next highest amount leading to EPS being unusually inflated. Using a 4 year CAGR from 2018, EPS has grown annually at 4%.

Latest results saw an increase in EPS of close to 12% in for the year 2022, with the increase in revenue and margin expansion showing on the bottom line.

From a returns point of view RELX has historically had a high return on invested capital, with the latest year being no exception at 17,5%. The last 10 years has seen ROIC close to 20% with it dropping below 15% only in 2020 during the pandemic. In addition to this return on equity is 46% with historically being around 50%.

Cash flow

As quality managers we look for companies that have a strong ability to convert its earnings into cashflow. RELX has historically excelled at this, with not only cash from operating activities being well above 100% but also free cash flow. RELX in the last year converted 24% of is revenue to free cash flows with 2014 being the last time the ratio was below 20%, proving the quality of their earrings .

RELXs capital expenditure consists mostly of expenditure on internally developed intangible assets, this is the amount spent on their various platforms and databases. Expenditure on property, plant and equipment is negligible. The other significant item in the investing section of is acquisitions of other businesses, RELX acquires bolt on acquisitions to further its offerings so it will not be surprising for this number to remain significant on the cash flow statement.

Balance sheet

A significant portion of the company’s assets, around 75%, are intangibles, with goodwill making up close to 70% of the number. With intangibles being this high it is important to assess it and determine if it could be a concern going into the future. We don’t see the level of intangibles being a concern for the following reasons:

Being a bolt on acquisitions type business, when RELX purchases additional subsidiaries there is a good chance that goodwill will be in the accounting recognition of the acquisition. RELX has a very broad range of services across a number of industries, this wide level of operations is due to years of business expansion, including acquisitions, this is why we are not surprised with the level of goodwill.

Non-goodwill intangibles are items such as datasets, customer lists and journals. Basically, any kind of right the company has to earn money off the use of the intangible asset. Per accounting standards the cost of these items need to be capatilised and amortised over its useful life.

Property, plant and equipment is negligible on the balance sheet, this is not surprising due to the operations of the company.

RELX has a total debt to EBITDA ratio of 2,24, this has come down from closer to 3 over the last 3 years, with total debt to assets of 40%.

One debt ratio that should be noted is the current ratio of 0,6. While it has improved over the passed few years we would be much more comfortable at a number over 1. Current ratio is current assets to current debt, current means less than a year. It in essence is a liquidity measure, a good rule of thumb is to have a ratio over 1.

The latest result showed interest coverage of close to 13 and free cash flow to debt of 30%, this with the debt maturity schedule being widely spread with most debt due after 2028 shows us that the debt levels are not excessive and RELX will be able pay it’s obligations when they come due.

Dividends

RELX is also a consistent returner of capital to shareholders. The dividend payout ratio has historically been around 60%. Dividends has grown at a CAGR of 7% over the last 5 years and over 9% in the last 3. We think this level of dividends is sustainable given the high level of cash generated from earnings.

RELX has implemented share buy back programs over the years, after significantly reducing buybacks in 2020 and using no cash for buybacks in 2021, 2022 saw £500 million used. Management in the latest results indicated to £800 million worth of shares will be bought back in 2023.

Future Growth

RELX is positioned well to benefit from the growing world of big data and machine learning, including AI. Data analysis is spreading across industries where in the past it was underrepresented, RELX is positioned well for this.

The sell side focus mostly on the final stages of the company’s transition to electronic from print format, which is expected to continue the expansion in margin in the near term. This margin expansion is expected to lead to increase EPS by low double digits over the next few years with revenue growing slightly less in high single digits.

ESG

We wouldn’t be surprised if while reading the above you would be thinking how does this fit into an ESG portfolio. While it is correct that RELX doesn’t provide a good or service directly related to ESG we believe it does fit into an quality ESG portfolio, and we do own it.

Firstly, like we have discussed in earlier posts, how a company operates is as important to the product they provide. RELX in this regard is highly efficient.

RELX currently has an MSCI rating of AAA, its highest rating, Morningstar has given it a negligible risk on it’s scoring system, it’s best score, and Bloomberg have rated it as a leader amount its peers in environment, social and governance criteria.

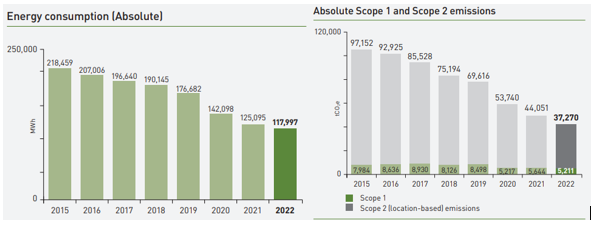

RELX is committed to operate as sustainable as possible, they have committed to the global plan to net zero and are annually lowering their carbon emissions.

In addition to the above, RELX makes it’s largest contribution to sustainability through it’s everyday provision of services. RELX provides the data and tools needs to inform debate, aid decision makers and encourage research and development in sustainability.

From the provision of services RELX provides, the following are examples of how they align with ESG.

Recent results from a study show that RELXs share of citations in environmental science represented 53% of the total market.

Within the Risk segment, more specifically the aviation analytics business, RELX provides carbon emissions capabilities to its comprehensive aircraft fleet analysis solutions, FleetAnalyzer. The tool and data allows for lessors and other industry participants to consider the carbon emissions of aircrafts in their fleet decisions. This tool provides one of the leading datasets on flight emissions.

In the Scientific, Technical and Medical segment, the company issues a report that tracks the relationship between health and climate change across a number of indicators. These reports look at how weather patterns, such as the heatwave seen in Europe last year, effect the community at large from aspects such as food security, housing security and the spread of infectious decisions.

What we can see from a company like RELX is that there are many other ideas for investments than the most held names in ESG investing. Another quick example is Dassault Systemes, a software company whose design tools are used for 80% of vehicles and 90% of aircrafts worldwide, one of their large clients is Tesla. The companies that provide the tools and data needed in the design and manufacture of the hardware used in the supply of sustainable goods and services in our view are as important and that’s where we think RELX fits in.

Governance

The CEO, Erik Engstrom, joined RELX as CEO of Elsevier in 2004, moving to CEO of the group in November 2009.

Under his leadership, RELX has transformed from a lower margin print business to a digital one, focusing more on higher margin analytical tools. This has been achieved through organic changes within the business and bolt on acquisitions over the last decade, something we think he has done quite successfully.

Looking at Glassdoor, RELX scores a good score of 78% when asking employees would they refer the company to a friend, this shows us that there is a good corporate culture at the company. Secondly, the CEO gets an approval rating of 85%, while obviously our view on the CEO is fundamental to the investment case, we also think it is important that a CEO has the support of their employees, which Erik Engstrom does.

The CFO is Nick Luff, he joined RELX in 2014, before this he was the CFO of Centrica Plc since 2007.

We think from a governance point of view RELX is in good hands for its shareholders. We also believe that their executive compensation is aligned with shareholder interest, their long term incentive targets include metrics such as cash conversion and ROIC, metric we ourselves significantly take into account.

Conclusion

RELX provide ESG investors with a good diversifier in their portfolios, while not really being considered a thematic or impact investment, the company operates exceptionally sustainably and it is because of that we believe it can be a good candidate for an ESG portfolio.

The company also fits well into our quality philosophy, it may not see high teen growth in the near term but its consistent revenue growth and margin expansion should provide shareholders with stable compounding return into the future.

If you have any comments, questions or suggestions please don’t hesitate to contact us. Follow us on Twitter and subscribe to keep up to date with all things Quality and ESG.

Thanks to Quality ESG Investing for highlighting RELX PLC (REL; REL LN).

(1) After reading your description of what REL does in its largest segment (risk), it seems like generative AI poses little risk to REL because most of REL's data is proprietary. What do you think?

(2) Have you considered Springer Nature AG & Co. KGaA (SPG; SPG GR)? It owns Nature journal, which is Elsevier's largest competitor.

I think SPG is interesting because of (a) under-recognised growth and (b) potential for higher capital returns. I discuss this in detail here: https://angsanaanderson.substack.com/p/shortlist-springer-nature-ag-and?r=5rl2u5